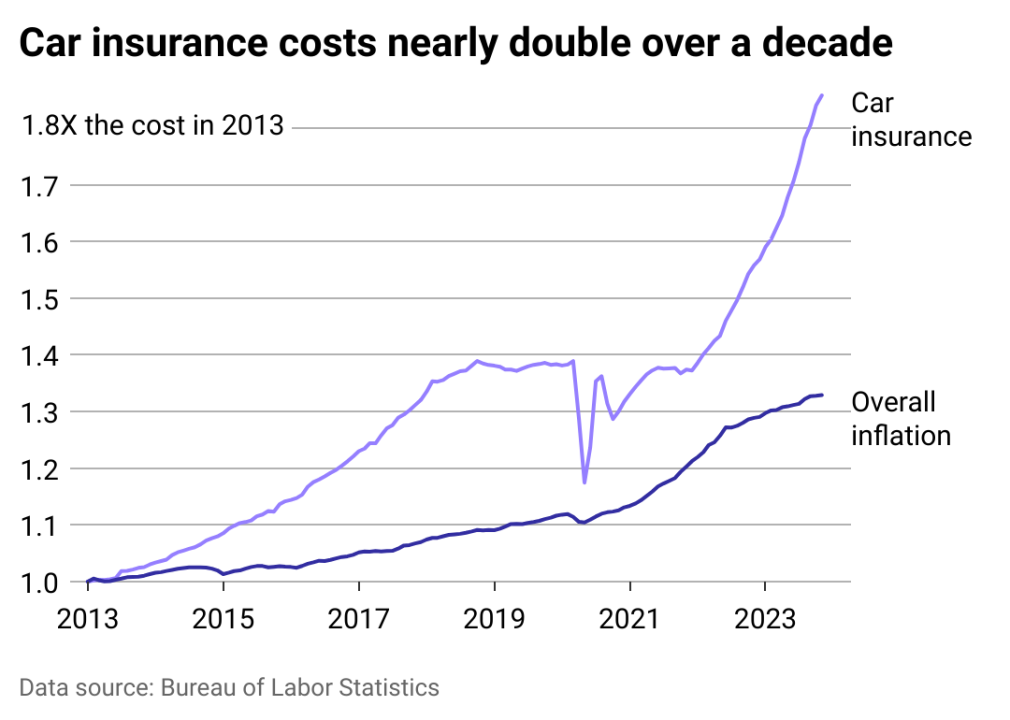

Car insurance costs have been on a steep climb, outpacing overall inflation by a significant margin. Data from the Bureau of Labor Statistics has shown that car insurance costs have risen at a much higher rate than other consumer goods and services. This trend is not a sudden anomaly but a reflection of a number of interconnected factors that have been impacting the automotive and insurance industries for years.

While the cost of new and used cars may be stabilizing or even decreasing, the expense to repair and insure them continues to rise. Insurers are facing an “underwriting loss,” meaning the money they collect in premiums is not enough to cover the claims they have to pay out. To compensate for these losses, they must increase premiums for all drivers. CheapInsurance.com identified the key reasons car insurance costs are rising faster than overall inflation:

1. Increased Frequency and Severity of Accidents

During the COVID-19 pandemic, fewer cars were on the road, but many drivers developed riskier habits, such as speeding and distracted driving. As traffic density returned to pre-pandemic levels, these behaviors persisted, leading to more frequent and severe accidents. More accidents mean more claims for insurers to pay, which directly drives up costs for everyone.

2. High Repair and Replacement Costs

This is a major driver of the increase in insurance costs. Several factors contribute to this:

- Complex Vehicle Technology: Modern cars are equipped with sophisticated technologies like cameras, sensors, and advanced driver-assistance systems (ADAS). While these features improve safety, they are expensive to repair or replace after a collision. A minor fender bender can now require a costly recalibration of these systems.

- Labor and Parts Shortages: The pandemic and ongoing supply chain issues have led to shortages of car parts, particularly microchips. This scarcity, combined with a shortage of skilled automotive technicians, drives up both the cost of parts and the cost of labor.

- Inflation: General inflation has increased the price of raw materials, parts, and labor for car repairs.

3. More Severe Weather Events

Climate change is leading to more frequent and intense natural disasters such as hurricanes, floods, and hailstorms. These events cause widespread vehicle damage, resulting in a large volume of costly claims for insurers to process. For example, a single hurricane can result in tens of thousands of auto claims. In states that are particularly vulnerable to these events, such as Florida, insurers are raising rates dramatically or even pulling out of the market entirely to mitigate their risk.

4. Rising Medical and Legal Costs

When accidents result in injuries, insurers are responsible for paying medical bills and legal settlements. The cost of medical care has been on a consistent rise, and an increase in litigation related to auto accidents also contributes to higher payouts. These costs are then passed on to consumers through higher premiums.

5. Increased Cost of Theft

While the cost of car theft may not affect insurance rates as much as accident claims, catalytic converter theft has become a nationwide problem. The cost to replace a stolen catalytic converter can be several thousand dollars, a cost that insurers must cover under comprehensive claims. This, too, contributes to the overall increase in premiums.

Frequently Asked Questions About Rising Car Insurance Costs

Why are car insurance rates increasing faster than inflation?

Car insurance rates are rising faster than overall inflation due to higher vehicle repair costs, expensive medical claims, and more severe accidents. Advanced technology in vehicles also increases the cost to repair and replace damaged parts.

Which factors are driving these cost increases?

Key factors include more frequent and severe accidents, higher medical and repair costs, increased vehicle values, and inflation affecting auto parts and labor. These elements all contribute to higher insurance claims and rates.

How can I manage or reduce my car insurance costs?

You can reduce car insurance costs by comparing multiple quotes, maintaining a clean driving record, raising your deductible, bundling policies, and qualifying for discounts for safe driving, vehicle safety features, or low annual mileage.

Story editing by Ashleigh Graf. Copy editing by Kristen Wegrzyn.