How auto insurance rates have changed over the past decades

QUICK ANSWER

Auto insurance rates have generally risen over the past several decades due to factors like increased repair costs for modern vehicles equipped with advanced technology. While the 1980s saw the steepest percentage hike in premiums, 2020 experienced a rare decrease as the pandemic reduced driving and accidents. However, the long term trend points to higher costs as insurers adjust for inflation, more frequent claims, and the rising price of medical care.

Auto insurance stands as a clear necessity for car owners. The cost often feels like a heavy financial burden. Personal factors like driving records age and vehicle type influence rates but the broader economic landscape plays a massive role too. Insurers look at collective behaviors to calculate risk. Increases in local accidents or complex vehicle technology cause rates to rise.CheapInsurance.com analyzed data from the Bureau of Labor Statistics Consumer Price Index to understand these changes since the 1970s.

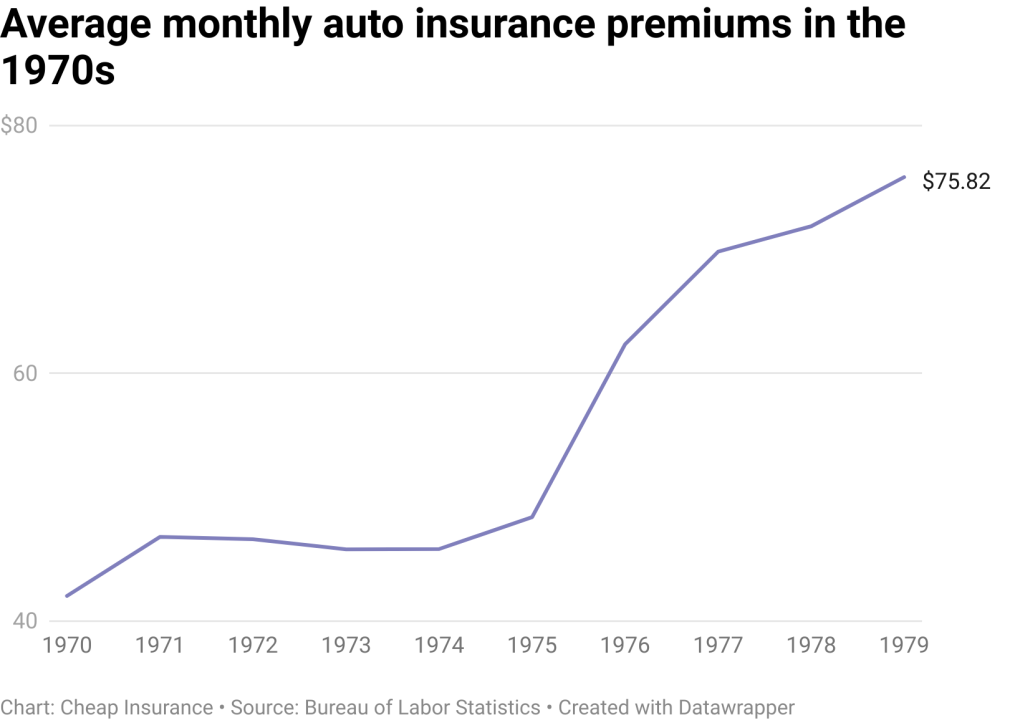

1970s

The 1970s marked a period of significant change for drivers and insurers. Rates began to climb as more cars hit the road and repair costs started to inch upward.

The Numbers

Average monthly insurance premium 56$

Premium increase from start of decade 34$ up 80%

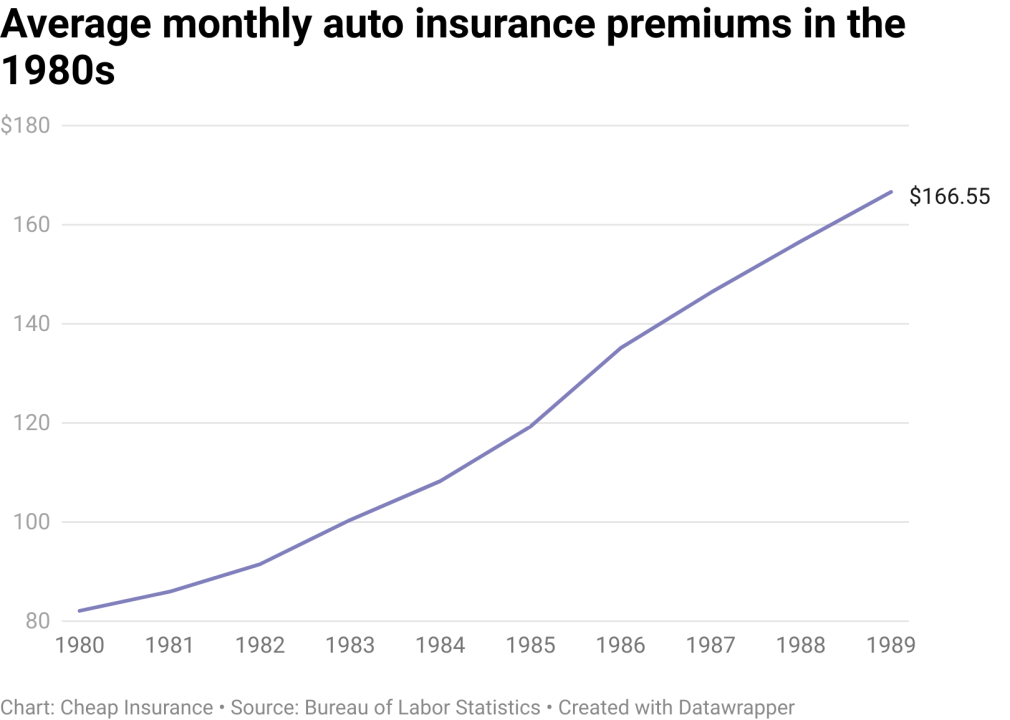

1980s

This decade witnessed the largest percentage increase in insurance premiums in the analysis. The average driver saw costs more than double between 1980 and 1989.

The Numbers

Average monthly insurance premium 119$

Premium increase from start of decade 85$ up 103%

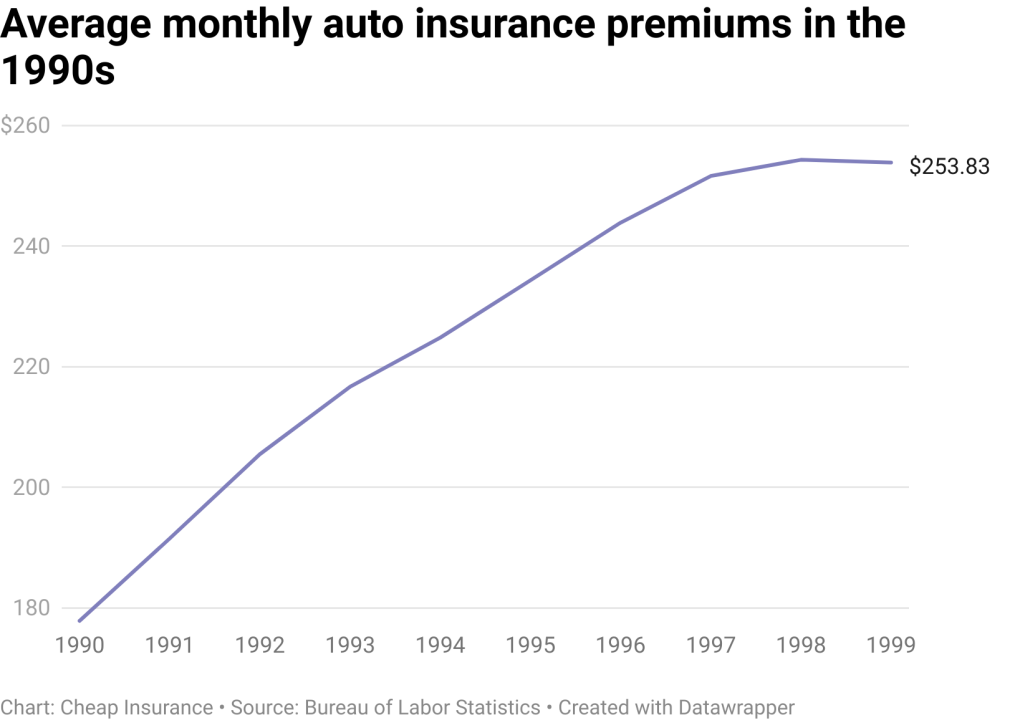

1990s

Technology began to impact the industry in the 1990s. Computers entered vehicles and insurers started using better data to price policies. The rate of increase slowed compared to the previous decade.

The Numbers

Average monthly insurance premium 225$

Premium increase from start of decade 76$ up 43%

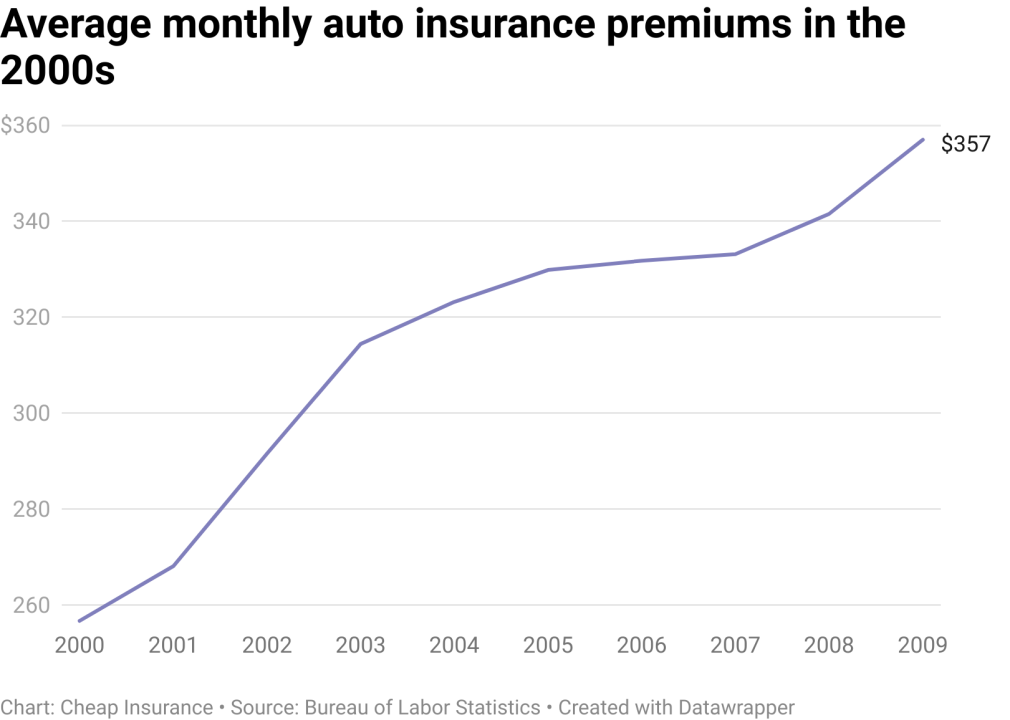

2000s

The new millennium brought more cars and more drivers. The rise of the internet also changed how people bought insurance. Rates continued to rise but the percentage jump remained lower than in the 80s.

The Numbers

Average monthly insurance premium 315$

Premium increase from start of decade 100$ up 39%

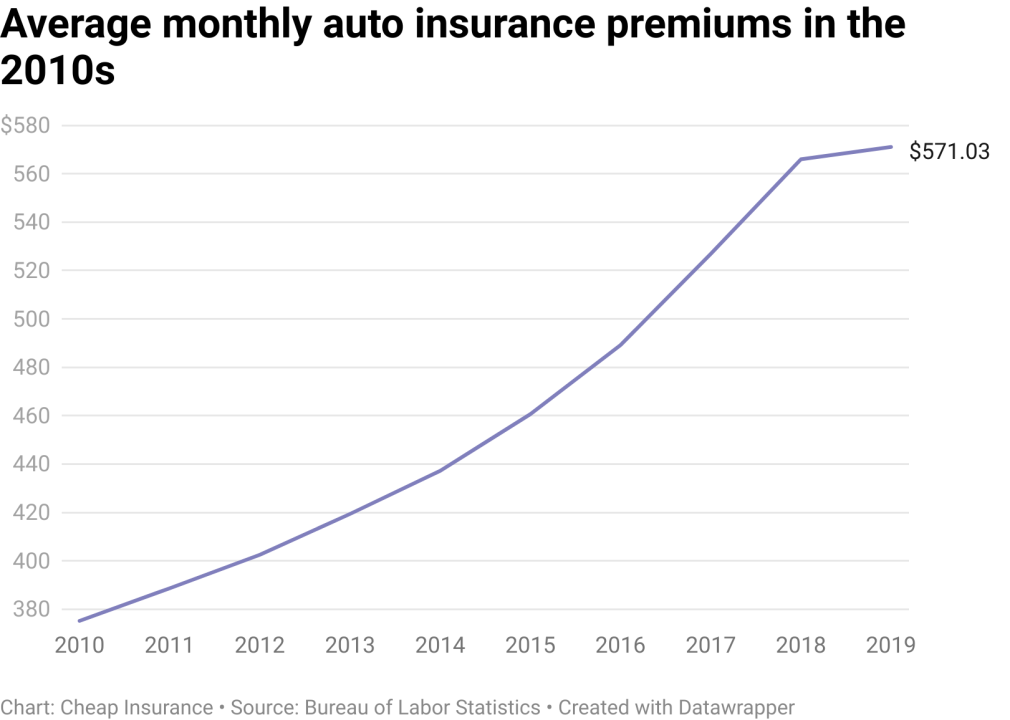

2010s

Smartphones and distracted driving became major issues during this time. Cars also became more complex which made repairs more expensive. These factors contributed to a steady rise in premiums.

The Numbers

Average monthly insurance premium 464$

Premium increase from start of decade 196$ up 52%

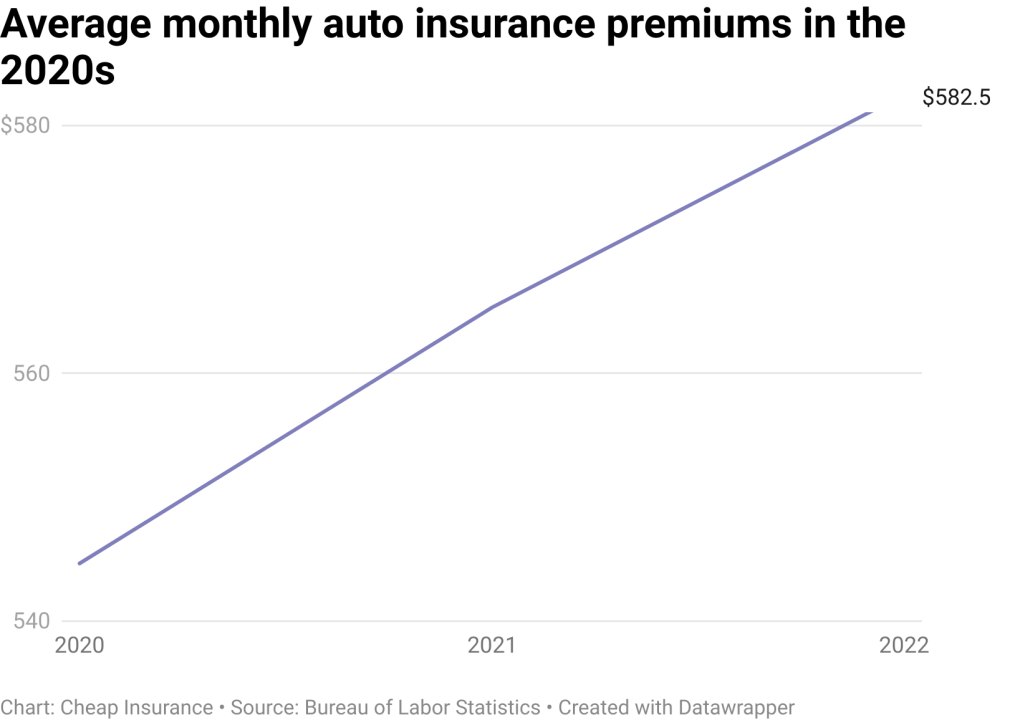

2020s

The current decade shows a unique trend. The year 2020 saw a significant decrease in rates due to the pandemic and fewer cars on the road. However recent years show a return to rising costs due to inflation and supply chain issues.

The Numbers

Average monthly insurance premium 564$

Premium increase from start of decade 38$ up 7%

Understanding the Trends

History shows thatauto insurance rates rarely stay flat. They react to the world around them.

Key Factors

Vehicle Technology Advanced electronics make modern cars safer but much more expensive to fix.

Economic Shifts Inflation and supply chain disruptions raise the cost of parts and labor.

Driver Behavior Distracted driving and accident rates directly impact the price of coverage.

Drivers today pay more in total dollars but the value of what insurance covers has also changed. Modern policies often protect against much higher liability risks and more expensive vehicle replacements than in the past.

Frequently Asked Questions About Auto Insurance Rate Changes

What factors have influenced auto insurance rates over the years?

Auto insurance rates have been influenced by inflation, medical and repair costs, vehicle technology, regulatory changes, and economic factors. Natural disasters, changes in accident frequency, and claims trends have also played a major role in rate fluctuations over time.

How have advances in vehicle technology affected insurance premiums?

Modern vehicles include advanced safety features and electronic systems, which can reduce accident severity but increase repair costs. These technological advancements have contributed to higher premiums for some vehicles due to more expensive repairs after collisions.

Can historical rate trends help predict future insurance costs?

While historical trends provide insight into factors affecting rates, future premiums depend on ongoing changes in claims, vehicle technology, regulatory policies, and economic conditions. Businesses and drivers should review coverage regularly and compare quotes to manage costs effectively.